Working from home is more hectic than working in the office. I have been procrastinating about updating my monthly budget because I bought (quite) a lot of stuff. I will lock the little shopping monster in the basement!

I’ve been owning my car for 3 years plus. Read my update last year here.

Year 03: 2019 / 2020

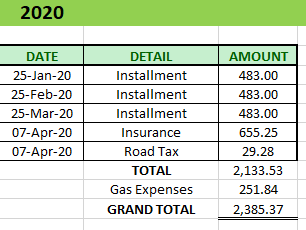

Total Year 3 of ownership;- RM8,649.80 (RM720.82 per month). Total cost for 3 years of ownership RM32,663.68 (RM907.32 per month). I had to recalculate it because I couldn’t believe it. But damage has been done, lesson learned. I’m going to drive it for as long as it will last and takes really good care of it. I still have RM23k of loan to serve. This is just for a local car. I couldn’t imagine how’s the number for an imported car. And I only drives it to work, fuel up once a fortnight (I have not been to a gas station for 2 months cuz that’s how long I’ve been working from home).

I took the moratorium to build up my Emergency Fund from previously 3 months to 5 months now. Short term plan is 6 months EF, ideally 1 year but the FD rate is just sad. I also put on hold my debt free plan and focus on investment instead.

I think by now most of us have heard about the viral story about a man who got scammed RM9,000 in six minutes. We can all learn a thing or two from his experience. Please do save the ATM / CC hotline of your bank into your phone. If your bank is not in the list, do search for it and save the numbers in your phone in case you cannot log into your online account to cancel the cards.

Public Bank (ATM Card) 603-2179 5000 (CC Visa / Mastercard) 603-2176 8555

Finally, after much consideration, I have decided to sell my last Unit Trust Regular Saving Plan (RSP) Fund. I don’t think it is suitable with my financial goals. Firstly, I like to see dividend rolling into my account (preferably on a yearly basis) and secondly, I don’t like paying the 3% sales charge anymore (and 1.8% management fees too). In the long run it just eats up on my capital and the return is not that good. One post that I saw on IG made me realize that. Do follow my IG below if you like to see me sharing random inspiring IG stories from others! Anyway, here’s a summary of my UT investment since 2015.

Considering the market outlook, I should be thankful I didn’t lose any capital. But like I said before, the return is not good. If I were to put the same amount into eFD, I’ll get more than that. And that is just the minimum 3%. But then again, I don’t have 5k when I started to invest. That amount grow from a monthly deduction of between RM104 – RM125. This can be a good way to force us to save some money, I guess, as it will auto-deduct from your account. Kinda like save and forget (and cannot touch too…)

Ouch

I will use this fund to buy some dividend stocks to build my passive income one ringgit at a time. Happy investing…

One night while being curious about how much money I have spend on H website, I’ve screen cap all my purchases (luckily they kept all the records) for self-reflecting purpose. It’s a good reminder for me to become more mindful with my spending. Anyway, read Part 1. 2017: Key word of the year “Stock” (no, not the ones from Bursa)

Feb 2017

Physiogel Lotion – I was searching for a lotion for my eczema that came out of nowhere.

Senka Perfect White Clay – One tube last forever about a year of almost daily usage.

Aug 2017: Kinda surprised I didn’t buy anything for 6 months.

L’Oreal Lotion – At that time I read about one product from the same line and wanted to try it but was not available in the market. Bought this to “try”. Just a normal lotion.

Nature Republic Aloe Vera – Sold this to a colleague in need.

Second purchase in Aug 2017

Nature Republic Aloe Vera – Bought this hoping that it will be able to help to sooth the itch from my eczema. Use it religiously for a while, until I got too lazy to transfer it from the big tub to a smaller container because of hygiene.

Miss Hana Brush Set – Wanted to start wearing eye shadow to office so I bought a set of cheap brushes to “practice”.

Senka Perfect Watery Oil – Since I use cleansing oil almost on a daily basis, I will buy any brands that’s on sale.

L’Oreal Lotion – Bought this as a gift.

Oct 2017

Miss Hana Brush Set – This is a good example of mindless shopping. Why did I get the same thing again?

Ryo Anti-hair loss Treatment – My fav treatment. I use this as a mask for my scalp for healthy scalp and hair regrowth.

A’pieu Healthy Scalp Doctor Tonic – Gives a minty feeling on scalp after spraying and massaging. But one bottle is not enough to see any result.

Second purchase in Oct 2017

Ryo Anti-hair loss Treatment – Stocking up when the price is low. You can get it from watsons now but it’s more expensive now (RM36 last checked in Aug 2019).

Got sucked into the Dec sales rabbit hole. First Dec 2017 purchase

Skin Food Rice Wash Off Mask – Pretty decent wash off mask. It smells so delicious.

Mise En Scene Perfect Repair – Bought this as a gift for Secret Santa.

Second Dec 2017 purchase

Dr. Morita Mask – I was running low on sheet mask and decided to try this brand because normally it’s quite expensive. (But after participating in L’Occitane’s recycling program, I think I’ll stop using sheet mask). Bought one set as gift and one set for myself.

Ryo Anti-hair loss Treatment – Stocking it up because at that time it isn’t available locally.

Third Purchase in Dec 2017

I’ve unlocked the shopaholic. The stock hoarding shopaholic that once was slumbering at the back of my lil mind. Oh no! 1. Dr. Morita Mask – More mask for the stock because it’s “cheap”. At that time I really think that way. That’s how sales can play with our mind.

Last purchase for 2017

Ryo Anti-hair loss Treatment – Stock while you can.

Mise En Scene – One for myself and one as a gift. I miss this brand from H site. It really makes my hair smooth and tangle free.

Actually I’m afraid to calculate the total for 2017 after reviewing my December purchases. But we have to face the cold harsh truth in order to learn from your mistakes. Here goes nothing. *drum roll* RM643.66 for 9 purchases (4 of it in December or 28.7%). And RM172.73 of it is gifts for others. On average RM53.65 per month, minus the random trip to local pharmacy. Favourite products from 2017 purchases;- Ryo hair treatment & Mise En Scene hair oil! Next up, 2018 purchases!

Do you consider taking care of your own skin as an investment? I’d like to think of it as an investment, at least in an abstract kinda way. That’s why previously I won’t hesitate to spend money to buy beauty products. At one point I was kind of proud becoming a Gold Member for H site. But after embarking in the whole debt free journey, I am more mindful with my spending. Now I’m in the midst of finishing up my stocks and in future will only buy essential stuff that works on my skin.

Anyway, let me just do a big beauty review of all the stuff I bought from H site since 2015 and mourn a bit for all the money wasted shopping instead of investing.

Year 2015 – 2016

First purchase Dec 2015. I guess I was attracted with the free gift

Miss Hana Eyeliner – I do not wear eye makeup *period*. Why, dear 4 years younger self, do you waste money on buying something you don’t use? I remember reading about it somewhere and wanted to try. Pretty waterproof.

3W Clinic Collagen Hand Cream – A normal hand cream. I got this to get the free shipping.

Second purchase: Feb 2016

Bioderma Toner – Best toner ever!!! A very moisturizing toner for me. The moment it hits your skin, it’s as if your skin is gulping it up. Love it but it’s too expensive.

Too Cool For School Oil Sheet – Bought it to get free shipping. Just a normal oil blotting paper that does the job.

May 2016

Yadah Starter Kit – Bought this because I was looking for something to combat my oily skin. Didn’t work for me.

Sulwhasoo Mini Care Set – Bought this set to try the first care activating serum and since made me a little fan of this product.

Petitfree eye mask – At one point I was crazy about eye mask but not discipline enough to do it on a daily or weekly basis thus no results.

B.liv Try Out Pack – Bought this to try the pore care thingy. To little to see any results.

Aug 2016

Sulwhasoo Mini Care Set – Wanted to try this series a bit longer.

Sulwhasoo First Care Serum – See, I’m a little fan of their First Care Activating Serum. It absorbs quickly into my skin and doesn’t make it oily. I have super duper oily skin. I hope I burn calories producing oil on my face.

Oct 2016: Just came back from Korea to buy more Korean stuff

Innisfree Super Volcanic Pore Clay Mask – Read great reviews about it but I think it breaks me out.

Ryo Anti-hair loss Treatment – I have fine hair genetic. A little bit of me die inside every time a hair-dresser reminds me about it (though they might no have any ill-intention). My hair has been shedding like crazy since forever but this treatment helps with the regrowth. Every week or so I have been religiously using this as a scalp mask. After shampooing, I will apply it generously on my scalp (yes, you can use it on your scalp) and leave it for 30 – 40 mins covered in a shower cap. And it will make your hair silky smooth.

Nov 16

Ryo Hambitmo Conditioner – I use conditioner on a daily basis, so bought this to try it out. For me it’s just a normal conditioner. I don’t have damaged hair to begin with.

Pascucci Cucumber Soothing Gel – Got this as free gift.

Nature Aloe Vera Mist – This is good for lazy people like me. I use this after washing my face because sometimes it feels kind of ‘tight’ after washing.

Dec 2016: Buying for the sake of free gift?!

Nature Republic Cleansing Oil – I use cleansing oil almost on a daily basis, and as I don’t have a preferred brand for it, I will buy when there’s promotion for it. I can say that it does the job well.

Nature Aloe Vera Mist – Bought this as a gift for my friend.

Holika Holika Beauty Bloody Oil Tint – My first and last oil tint from tint craze time. It’s hard to clean and still sitting in my drawer.

7 purchases in year 2015 / 2016. Total damage RM446.70 (RM38 p/m). After going through all my purchases, there are only 3 items that I really like;- Bioderma Toner, Ryo Anti-hair loss treatment and Sulwhasoo First Care Activating Serum.

I want to recycle all these but I can’t find a way to do it until now.

Accidentally found out about this campaign while I was googling about one of the product that I want to try. And I can exchange for the 5 ml sample if I recycle 18 full-sized beauty product packaging, the best part is they accept any brands. At first I was kinda lazy to do that because I thought I have to bring in 18 empties, but I was wrong. You will receive a travel size product by L’Occitane for every 6 full-sized empties that you recycle.

So I spend one weekend morning cleaning and sorting out all the empty bottles in my house. I want to recycle it but I can’t find a way to do it until now.

I hope this will be able to help give you a rough idea on what can be recycled in this program. Just make sure they are clean and dry

a) Beauty Packaging Shiseido Aqualabel Deep Clear Oil Cleansing – 150 ml x 1 b) Skin Care Packaging Johnson’s pH 5.5 Nourishing Body Wash – 1000 ml x 2 Johnson’s pH 5.5 2 in 1 body wash – 750 ml x 1 Guardian Mediterranean Grape Seed Oil Body Wash – 470 ml x 1 Iope Bio Essence Intensive Conditioning – 168 ml x 2 Guardian’s Aloe Vera Gel – 250 ml x 1 Hada Labo Arbutin Whitening Essence – 30 ml x 2 Innisfree Jeju lava seawater intensive Ampoule – 30 ml x 1 Skinfood Rice Mask Wash Off – 100 ml x 1 Laneige Multiberry Yogurt Repair Pack – 80 ml x 1 The Face Shop Chia Seed No Shine Hydrating Cream – 50 ml x 1 Physiogel Lotion – 200 ml x 1 c) Hair Care Packaging Ryo Hair Strengthening Shampoo – 400 ml x 1 Wowo Pure Ginger Shampoo – 300 ml x 1 Watson’s Hair Strengthening Shampoo – 400 ml x 1 Ryo Hair Loss Care Treatment – 300 ml x 1 Pantene Conditioner Hair Fall Control – 180 ml x 1

Not counted but they will accept it to be recycled. Dr. G White Aura Lotion – 140 ml x 1 (Min volume 250 ml for toner) Loreal Hydrafresh Anti-Ox Spa Water – 130 ml x 1 (same as above) Tsubaki Volume Touch Shampoo – 200 ml x 1 (Min volume 250 ml for shampoo)

Did a rough calculation of the products above and it comes to a total RM1250,78. OMG!

Seeing all the waste that I have accumulated in one year or two, it makes me wonder about all the ones that I’ve tossed out all my life. I wouldn’t mind not being rewarded for recycling because I know I can take a small part in reducing the waste filling the landfill. For more info about this program, go to;- Big Little Things website.

This is one of my favourite account since my pre-budget days because it’s one of the few savings account out there that pays interest on a monthly basis (latest interest rate is 1.85% p.a.). I think the reason I like it is because we can open an account conveniently online and interest is paid in a monthly basis with no other annoying conditions except to have RM2,000 in the account.

Pros and Cons + Can open an account conveniently online. + Earn 1.85% interest p.a. if you have at least RM2,000 in the account. For example you can choose to bank in your salary into this account and earn some interest in the beginning of the month before spending it since interest is calculated daily. – There are minimum savings requirement of RM250. – When you withdraw money from ATM, you cannot use Fast Cash option if you want to withdraw from your M2u Savers / Savers-I account. +/- For debit card you can choose the free option but limit to 4 withdrawals per month (or pay RM0.50 per withdrawal thereafter) or pay RM8 for unlimited withdrawals.

Can we apply for both M2U Savers and M2U Savers-i? From my own personal experience, the answer is yes! I currently have both account for different purposes. One is for my Sinking Fund and another is for my Early Exit Fund.

With the flexibility of having two interest-bearing account, I will be able to keep track on the in-flow and out-flow for each of them instead of having them mixed up and I’ve learned from experience that mental calculation doesn’t work, at least for me. That’s all the sharing for today. I hope it will be able to help. Small Income Big Dreams

Goal for this year is to get RM1,500 from interest & dividend. Every little bit counts for me. #SmallIncomeBigDreams

This has been a slow year.

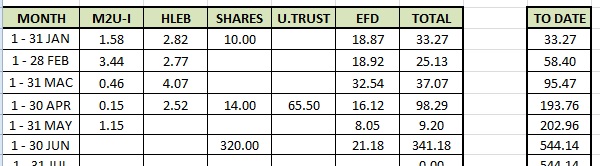

First post about this, let me do some explanation. M2u-i: For “Sinking Fund” (Travel, car maintenance, impulse purchase, “parking” Emergency Fund until it’s enough for EFD placement). Some of the interest from my EFD will go to this account as well. HLEB: I will transfer a set amount monthly to buy stocks when the price is right. It pays interest if you have a minimum of RM1,000. Shares: Dividend from stock. U.Trust: The first investment I did. I have 2 different unit trust with MBB and one PRS. Each counter is supposed to pay dividend but only received dividend from one counter. Last check still no paper lost. (Thankfully) EFD: My Emergency Fund. Now just 50% of my 6 months expenses target. I try to set so that the interest is added into the principle. But some won’t let me do that.

Mid Year review This year’s progress has been slow for both investment and dividend. Initially for this year I planned to invest RM10,000 before discovering the Debt Free Community. Right now I’m focusing on eliminating my consumer debt (Hire Purchase) before concentrating on my investment so I can put more fund to it but I will still put a small percentage of my salary into investment.

Investment Progress up until June 2019 JAN – MAR (RM1,350) Can read from my IG post. APR – JUNE (RM1,286.50) APR Trust account: RM50 RSP: RM125 Dividend: RM79.50 MAY Trust account: RM587 PRS: RM125 JUNE Dividend: RM320 Total JAN – JUNE 2019: RM2,636.50 (26.4%) from my RM10,000 goal.

“Slow progress is better than no progress.” -Unknown.

Failing to plan is planning to fail. -Benjamin Franklin.

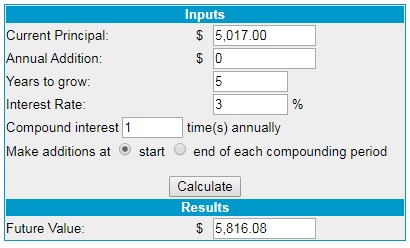

Read my previous post about new car ownership cost for 2 years. My goal now is to cut short the tenure from 7 years to 4 – 4.5 years and save at least RM900 – RM1,300. The figure might not sound a lot but money saved here is fund that could be used somewhere else instead.

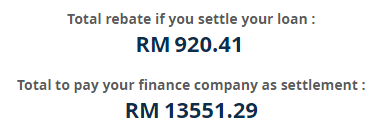

Got this figure from AutoWorld if I settle it in 2.5 years

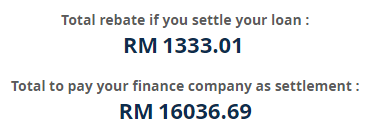

The figure if I settle it in 2 years

The Plan and Loan Balance Duration: 24 – 30 months / 60 months (By June 2021 – Dec 2021) Loan Balance: RM27,461.70 / RM33,000 (As of June 2019) Amount to pay per month: RM483 Amount to save per month: RM667 (2 years) / RM450 (2.5 years)

The Plan I will continue paying the monthly installment. As for the extra payment, I will transfer it to an interest-bearing account (M2u Savers) and save until I have enough to settle it within my time-line. For start, I will put RM500 into this account every month and any extra money I have left from my monthly allowance. Hopefully in 2 – 2.5 years I’ll be able to save up RM16,000 to settle my loan in one go. I will have to pay the full RM27k if I follow my original plan. Got some advice from one of my IG post about car extra payment. (Thank you!!!)

Motivation I think it helps a lot to post your progress online. For instance, I created an IG account (@AiryLilM) and this blog solely for this purpose and to connect with like-minded individuals and get inspired by their stories and journey, they are one of the reason I’m determined to cut short my loan tenure. Been a silent reader for years before I stop procrastinating about starting to jot down my journey. I hope 10 years later I can look back and say I’m glad I started to plant my little tree.

My little advice to those who wanted to do the same. 1) First, START. It’s the hardest part but don’t procrastinate. 2) Track your expenses, I’m using MoneyLover because I can see how much money I can spend before going over-budget. You can set a reminder if you’re the type that tend to forget about it. 3) Do a budget after payday and update your progress for previous month. I follow a zero-based budget where the Total Debit each month will be the same as my Net Salary. Key to success is to not strain yourself. Tighten your belt bit by bit and do not go cold turkey!

Here’s my template. Feel free to save and adjust accordingly

4) Set your plan. Big plan (eg to settle PTPTN loan in X years) and break it into little parts with action plan (To pay Y amount per month). Again, don’t strain yourself. Set an amount that you’re comfortable with but make sure it’s higher than your monthly interest. 5) Be consistent. At first the progress will be slow but with consistency it will be possible.

I wish we have shows like this in Malaysia cater to Malaysian audiences. Sadly it’s only in Cantonese (sorry guys). I will try my best to summarize the content of this show.

This episode features a 25 year old girl who wants to save HK$80,000 (4 times salary) to help her family with their renovation cost and for long term would like to have a capital of HK$300,000 (15 times salary) in 3 – 4 years to expand her business to become an established online business.

She then list down her monthly expenses, coming to around HK$12,800 (largest expenses being credit card repayment at around HK$4,000 or 20% of salary). Her salary is in the range between HK$15,000 – HK$20,000. To achieve her goal, she has to save between HK$5,000 – HK$7,000 a month, roughly 25% – 35% of her salary.

So for a week she has to track her expenses and limit her spending to HK$100 a day (0.5% of salary). She has to limit her credit card spending and pay cash instead. The PF guru also advise her to start working on her online shop instead of waiting until she has enough capital. And the most important thing is to find your own niche in the market because there are a lot of people doing the same thing. Do not try to be the best but try to be the most unique.

What we can learn 1. It’s important to start. Do not hesitate. 2. Set a daily budget for yourself and stick to it. 3. Curb impulsive purchase especially with credit card. Use cash from your daily budget.

I watch a lot of finance related documentaries in Youtube. I guess I just like to see things from different perspectives and sometimes count my blessing as I think our situation is better even though we’re living in a developing country. Enough knowledge sharing for today.